We, at Khor Reports, recently attended a conference in Singapore that was largely concerned with deforestation in SE Asia. It was a well attended event, with representatives from the Norway and Indonesia governments, a video from the UN's forest secretariat and a strong presence from key environmental NGOs, a few with 100-year histories (information about the conference here: http://web1.iseas.edu.sg/?p=4977). The latter presented some information about their REDD+ projects. These seek to bring other incomes to local peoples, to give them an alternative to agriculture extensification i.e. cutting down trees and planting crops such as palm oil.

Market perversion, with 10-20% to local peoples / farmers

A crucial question from the audience was left unanswered in the public forum. A professor asked how much money actually goes to the local community and how much to bankers, consultants and other facilitators (I paraphrase). We all, should be concerned about how much in the $1 goes to the different parties involved in sustainability efforts.

So, let's take a look at the Roundtable for Sustainable Palm Oil's (RSPO) Certified Sustainable Palm Oil (CSPO) at GreenPalm (the book and claim system). At present, the price for CSPO certificates is US 25 cents (down from USD40 or so), and the brokerage fee is USD1.50 and the fee to the RSPO is USD1.00 (source:http://www.greenpalm.org/en/faqs/general#how-much-are-brokerage-fees). Thus, a buyer of 1 mt of this sustainable palm oil would pay a premium of USD2.75. In effect, 9% of the premium goes to the planter of palm oil and 91% goes to the facilitators (GreenPalm and the RSPO)#.

This is the opposite of what we would expect. We all would like to see the bulk being earned by the local peoples / farmers i.e. the 'doers'. In reality, the opposite is the case. Thus, it is a perversion of the so-called market (MS Word's thesaurus likens 'perversion' to the words parody, caricature, distortion, falsification, twisting, slanting...).

Is the current RSPO GreenPalm situation uncommon? Unfortunately, it seems to be consistent with the feedback that various sustainability efforts may only pay 10-20 cents in the dollar to the local doers / peoples. Perhaps a key problem is the collapse of voluntary market prices for many types of sustainability credits and certificates (and the outlook isn't good, given the economic troubles ailing the developed world). Other problems could be sub-optimal structuring of the projects and that too many parties are involved, with each seeking some upfront and fixed payment that is not tied to the price and performance of the traded certificate.

Good practices - 3 lessons from the NGO sector

We should ask this: what is good practice? Let's learn from the NGOs. They are often judged by the amount that they spend on their projects vs. what they spend on administration and fund raising. A common target threshold is some 85 cents in the dollar going to project or program work.

Take a look at Oxfam Hong Kong's 'Use of Donations' statement here, http://www.oxfam.org.hk/en/useofdonations.aspx. Another good practice for NGOs is the local sourcing of funding with low / no reliance on overseas HQ and government funding. This vastly improves a charity's autonomy. Along this vein, Khor Reports ventures to suggest more good practices: a wide breadth of funding, especially from individuals and less from corporates, and with 'limits' on single-source funding to avoid 'capture' by particular interests. Oxfam also says that for emergency efforts, "ALL donations – exactly 100% – go to assist people in need."

Thus, the palm oil sector could draw three (3) lessons for its sustainability programs: i) target no more than 15% on facilitation costs, ii) aim to localize and be autonomous, while avoiding capture by special interests and iii) for special worthy cases e.g. independent smallholders, zero facilitation costs.

Fix it

Thus, NGOs offer lessons in good practices. Clearly, NGOs should replicate such practices when designing and implementing projects affecting local peoples in developing countries. We hope to see that most of their programs deliver 85% benefits to the local peoples / farmers. These are the people nearer the bottom of the 99% that the Occupy Wall Street demonstrators are telling the 1% (the rich) not to forget. They say "the system is broke," and we at Khor Reports recognise in this statement, two meanings of the word "broke". So, let's not have socio-environmental efforts become another financial tool of (or captured by) rich interests. Let's fix it.

#In this, we have not even considered the direct and indirect costs of certification (the former estimated at USD6-12 per mt for corporate planters).

This blog highlights news and views on markets, marketing, sustainability and political-economics of palm oil. Any views belong to the respective authors and do not represent that of any particular organization. I update this in my spare time. Since mid-2016, the more "comprehensive" news is available on customized request. Market news and big news continue to be updated. Thank you for reader interest that has generated over 130,000 page views in 2016.

Friday, October 21, 2011

Wednesday, October 12, 2011

Palm oil on fast-track vs. others

The Star reports, October 11, 2011, "Demand for certified sustainable palm oil surges 70%":

RSPO president Jan Kees Vis said in a statement that “the current number sparks hopes that a breakthrough is near.”“Historically, there has always been a delay in market take-up versus production increase, as buyers of large companies have to commit as long as a year in advance to buy raw materials,” he said. “They will only sign on to what they are sure they can actually purchase from the market in the future,” he added. Secretary-general Darrel Webber also noted that “a significant number of retailers, consumer goods manufacturers, processors and traders have committed to 100% CSPO by 2015.”..........

Khor Reports comment:

a) The increase in market off-take to 70% from its recent plateau at 50% will surely be welcomed by producers of CSPO. Perhaps buyers have been reacting to the recent flap at RSPO: the withdrawal of GAPKI and the call associated with MPOA for a 3-year moratorium on certification (but with no corporate reactions yet).

b) Sometime ago, Unilever said that they accounted for some 50% of CSPO purchases. As the lead product manufacturer in RSPO, perhaps Unilever stepped up its buying recently? This company is one of the key drivers of the agriculture sustainability sourcing via the WWF-driven 'roundtables schemes'.

c) Let's take a quick look at Unilever's commitments on sourcing sustainable inputs. The graphic below shows that palm oil is on the fast-track with a 'by 2015' target, while other competing oils will be sustainably sourced only by 2020. Moreover, news reports say that Unilever seeks to replace palm oil in its Dove soap and lotions within a few years. In this regard, palm oil has been selected as the oil most in urgent need of sustainable requirements (and some replacement).

d) The palm oil fast-track by buyers has only been exceeded by the fast-track that growers have taken in providing RSPO CSPO to the market. With the recent sharp rise in CSPO, it appears that palm oil is some 7-9 years ahead of its competitor oils - soybean oil, rapeseed oil and sunflower oil.

e) This assumes that many manufacturers also use Unilever's timeframe and that the other oil growers take a more moderate approach e.g. the more business-friendly RTRS / soy roundtable allows for partial certification while RSPO requires rapid or 'challenging' timeframe for 100% certification.

RSPO president Jan Kees Vis said in a statement that “the current number sparks hopes that a breakthrough is near.”“Historically, there has always been a delay in market take-up versus production increase, as buyers of large companies have to commit as long as a year in advance to buy raw materials,” he said. “They will only sign on to what they are sure they can actually purchase from the market in the future,” he added. Secretary-general Darrel Webber also noted that “a significant number of retailers, consumer goods manufacturers, processors and traders have committed to 100% CSPO by 2015.”..........

Khor Reports comment:

a) The increase in market off-take to 70% from its recent plateau at 50% will surely be welcomed by producers of CSPO. Perhaps buyers have been reacting to the recent flap at RSPO: the withdrawal of GAPKI and the call associated with MPOA for a 3-year moratorium on certification (but with no corporate reactions yet).

b) Sometime ago, Unilever said that they accounted for some 50% of CSPO purchases. As the lead product manufacturer in RSPO, perhaps Unilever stepped up its buying recently? This company is one of the key drivers of the agriculture sustainability sourcing via the WWF-driven 'roundtables schemes'.

c) Let's take a quick look at Unilever's commitments on sourcing sustainable inputs. The graphic below shows that palm oil is on the fast-track with a 'by 2015' target, while other competing oils will be sustainably sourced only by 2020. Moreover, news reports say that Unilever seeks to replace palm oil in its Dove soap and lotions within a few years. In this regard, palm oil has been selected as the oil most in urgent need of sustainable requirements (and some replacement).

d) The palm oil fast-track by buyers has only been exceeded by the fast-track that growers have taken in providing RSPO CSPO to the market. With the recent sharp rise in CSPO, it appears that palm oil is some 7-9 years ahead of its competitor oils - soybean oil, rapeseed oil and sunflower oil.

e) This assumes that many manufacturers also use Unilever's timeframe and that the other oil growers take a more moderate approach e.g. the more business-friendly RTRS / soy roundtable allows for partial certification while RSPO requires rapid or 'challenging' timeframe for 100% certification.

Friday, October 7, 2011

MPOA calls for halt to new RSPO certification?

“We want to see the current RSPO certified palm oil production of 5.1 million tonnes be fully taken up by Western buyers,” said MPOA vice-chairman Boon Weng Siew. Of the total RSPO-certified palm production, MPOA claimed that only 40% was taken up while the CSPO premium had plunged to only 30 US cents compared with US$50 per tonne in 2008.... Bek-Nielsen...said the world palm oil producers must unite and stressed that “We should not certify any new production units unless demand matches the supply of CSPO. It is time for the end-users to live up to their rethorics.”... An industry member of MPOA said the association might seek for a three-year moratorium to stop Malaysian planters from pursuing their on-going RSPO certification at the RSPO 9th Annual Meeting Roundtable in Sabah next month....“We will strongly push for this agenda,” he said. This is in view of the pledges given by Western food and consumer goods to use only CSPO in their operations by 2015.... reports The Star, 6 Oct 2011, "Malaysian Palm Oil Association won’t quit Roundtable on Sustainable Palm Oil," http://biz.thestar.com.my/news/story.asp?file=/2011/10/6/business/9638574&sec=business.

Khor Reports comment: Hot on the heels of last week's pullout from RSPO by GAPKI, Malaysia's key producer association affirms its membership, but calls for a halt to new certification. There has been a small glut in RSPO CSPO or certified sustainable palm oil, as the enthusiasm of producers for this sustainable product has not yet been met by sufficient buyer interest. Last year, we at Khor Reports speculated in our newsletter #2 that producers might seek to clear the overhang, but we had no idea then what might be the mechanism (download our report and refer to page 6, Option E: https://sites.google.com/site/khorreports2011/palmoil_strat_analysis/khorreport002-palm_oil-rspo_growers-100826.pdf?attredirects=0&d=1). It will be interesting to look out for corporate reactions to the recent moves by GAPKI and MPOA.

For more background, please refer to other postings in this blog, and Khor Yu Leng's article in Lipid Technology, "The oil palm industry bows to NGO campaigns," May 2011, http://onlinelibrary.wiley.com/doi/10.1002/lite.201100106/abstract.

Khor Yu Leng was interviewed for today's The Edge Daily: "Independent agribusiness analyst Khor Yu Leng, who has tracked sustainability certification practises, says oil palm players cannot be blamed for wanting a more level playing field with other types of vegetable oil producers. “RTRS, the standard for sustainable soybean, is more business friendly versus the RSPO, despite their being sister organizations,” she said. She thinks the palm players will move towards having more than one type of certification, to meet different market needs."

Khor Reports comment: Hot on the heels of last week's pullout from RSPO by GAPKI, Malaysia's key producer association affirms its membership, but calls for a halt to new certification. There has been a small glut in RSPO CSPO or certified sustainable palm oil, as the enthusiasm of producers for this sustainable product has not yet been met by sufficient buyer interest. Last year, we at Khor Reports speculated in our newsletter #2 that producers might seek to clear the overhang, but we had no idea then what might be the mechanism (download our report and refer to page 6, Option E: https://sites.google.com/site/khorreports2011/palmoil_strat_analysis/khorreport002-palm_oil-rspo_growers-100826.pdf?attredirects=0&d=1). It will be interesting to look out for corporate reactions to the recent moves by GAPKI and MPOA.

For more background, please refer to other postings in this blog, and Khor Yu Leng's article in Lipid Technology, "The oil palm industry bows to NGO campaigns," May 2011, http://onlinelibrary.wiley.com/doi/10.1002/lite.201100106/abstract.

Khor Yu Leng was interviewed for today's The Edge Daily: "Independent agribusiness analyst Khor Yu Leng, who has tracked sustainability certification practises, says oil palm players cannot be blamed for wanting a more level playing field with other types of vegetable oil producers. “RTRS, the standard for sustainable soybean, is more business friendly versus the RSPO, despite their being sister organizations,” she said. She thinks the palm players will move towards having more than one type of certification, to meet different market needs."

Felda listing mooted again

Two articles on Felda in the print and online news today.

a) Felda commercial arm to list? It will create world’s largest listed plantation firm, http://biz.thestar.com.my/news/story.asp?file=/2011/10/7/business/9648450&sec=business

b) Concerns at Felda's Coop, http://www.malaysia-chronicle.com/index.php?option=com_k2&view=item&id=20674:isa-samad-makes-his-move-but-felda-settlers-call-for-his-removal-as-co-op-chief&Itemid=2

Khor Reports comment: Rumours of the listing of Felda Group or one of its key entities have recurred over the years. The Group, controls some 850,000 Ha of both settler and commercial land bank. For a long time, it has been the largest plantation in SE Asia, if not the world (if one excludes the fluctuating figure of the unplanted reserves of the likes of Sime Darby and Golden Agri). It grew out of a land resettlement scheme, under the Federal Land Development Authority. What has held up a listing of a Felda unit for decades? After all, Malaysia is well known for privatizations and public-listings of government-linked entities. The key issue is this: majority ownership is held Koperasi Permodalan Felda or KPF (website: http://kpf.felda.net.my/Pages/kpf.aspx). Under a cooperative, key corporate actions would require that settlers and staff of Felda (current and former?) who are members of KPF, would have to vote on it, on the "one man, one vote" basis.

Interviewed by The Edge in January 2011, "Taking Felda to the next level,"

http://www.feldaholdings.com/content.php?h=4177&lang=EN.

a) Felda commercial arm to list? It will create world’s largest listed plantation firm, http://biz.thestar.com.my/news/story.asp?file=/2011/10/7/business/9648450&sec=business

b) Concerns at Felda's Coop, http://www.malaysia-chronicle.com/index.php?option=com_k2&view=item&id=20674:isa-samad-makes-his-move-but-felda-settlers-call-for-his-removal-as-co-op-chief&Itemid=2

Khor Reports comment: Rumours of the listing of Felda Group or one of its key entities have recurred over the years. The Group, controls some 850,000 Ha of both settler and commercial land bank. For a long time, it has been the largest plantation in SE Asia, if not the world (if one excludes the fluctuating figure of the unplanted reserves of the likes of Sime Darby and Golden Agri). It grew out of a land resettlement scheme, under the Federal Land Development Authority. What has held up a listing of a Felda unit for decades? After all, Malaysia is well known for privatizations and public-listings of government-linked entities. The key issue is this: majority ownership is held Koperasi Permodalan Felda or KPF (website: http://kpf.felda.net.my/Pages/kpf.aspx). Under a cooperative, key corporate actions would require that settlers and staff of Felda (current and former?) who are members of KPF, would have to vote on it, on the "one man, one vote" basis.

Interviewed by The Edge in January 2011, "Taking Felda to the next level,"

http://www.feldaholdings.com/content.php?h=4177&lang=EN.

Monday, October 3, 2011

RSPO vs. soy roundtable

News: GAPKI, the key palm oil producer association of Indonesia withdraws from its membership and its Executive Board role in the RSPO. Source: http://www.rspo.org/?q=content/statement-gapki%E2%80%99s-withdrawal-rspo.

Khor Reports comment: There had been market rumours. Also, the growers' collective dissatisfaction with RSPO is well known. But, seeing is believing. It has happened; Indonesia is following the play book that Brazil has also used. Read about it here in our Khor Reports, Palm Oil Strategic Analysis newsletter #2: https://sites.google.com/site/khorreports2011/palmoil_strat_analysis/khorreport002-palm_oil-rspo_growers-100826.pdf?attredirects=0&d=1.

Since the subject of soy crops up, let's do a quick comparison of some of the key features and achievements of RSPO and its sister organisation in the soy sector, the Roundtable for Responsible Soy (RTRS). RSPO and RTRS have some common Executive Board members - including WWF and Unilever.

Summary info

RTRS: Initiation of consultation in 2004, first certification c. June 2011. Current price of certificates is USD5. 90,500 ha currently certified.

RSPO: Initiation of consultation in 2002, first certification c. end 2008. Current price of certificates is USD1. Over 1 million ha currently certified and 2.6 million ha promised in timebound plans by 2020.

Partial vs. full certification

RTRS: A producer can certify part of his production, but for his entire production area, he needs to implement some fundamental criteria e.g. not to deforest HCVA in non-certified areas. It is up to the producer to determine how much market demand there is for certified soy, so no specific percentage for certification is required (i.e. partial certification is OK).

RSPO: Since Nov 2008, growers have to timetable their adoption plans. Producers have to submit time-bound plans for their certification efforts; they are required to certify all their mills & supply bases (i.e. full / 100% certification is required). Clause 4.2.4 states: “A challenging time-bound plan for certifying all its relevant entities is submitted to the Certification Body (CB) during the first certification audit.” Source: “RSPO Certification Systems, Final document approved by RSPO Executive Board, 26 June 2007, Approved by Executive Board on 3 March 2011 on Revised clause 4.2.4.”

Principles & criteria

RTRS: 5 principles, 28 criteria, 95 indicators.

RSPO: 8 principles, 39 criteria, 118 indicators.

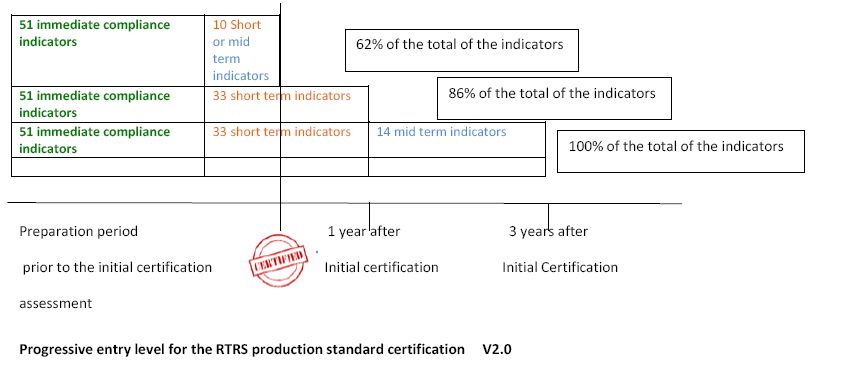

Phase-in compliance

RTRS: Gives producer 3 years to phase-in compliance. Allows partial compliance of 62% in year 1 and 86% in year 2, prior to 100% compliance in year 3.

RSPO: Phase-in not available.

HCV assessments

RTRS: Not required if expansion of soy cultivation is a) in line with an RTRS-approved map and system, or b) in non native forests areas and official land-use maps zone those areas for expansion or c) it is outside priority conservation areas.

RSPO: An HCV assessment, including stakeholder consultation, is conducted prior to any conversion. Also, refer to List of RSPO approved HCV assessors.

A quick glance indicates that on several fronts, RTRS is not as tough as RSPO. RTRS Standards also appears to better drafted, with a better categorisation of the P&C typology - this means fewer overlaps and confusions. When it comes time for RSPO to review its P&Cs (by 2012), it might look to the RTRS as an example.

Despite the more 'business-friendly' look of RTRS (vs. RSPO), Brazil soy association interests withdrew from RTRS. Brazil soy is slated to launch its own industry-led sustainability certification system, called "Soja Plus".

Khor Reports comment: There had been market rumours. Also, the growers' collective dissatisfaction with RSPO is well known. But, seeing is believing. It has happened; Indonesia is following the play book that Brazil has also used. Read about it here in our Khor Reports, Palm Oil Strategic Analysis newsletter #2: https://sites.google.com/site/khorreports2011/palmoil_strat_analysis/khorreport002-palm_oil-rspo_growers-100826.pdf?attredirects=0&d=1.

Since the subject of soy crops up, let's do a quick comparison of some of the key features and achievements of RSPO and its sister organisation in the soy sector, the Roundtable for Responsible Soy (RTRS). RSPO and RTRS have some common Executive Board members - including WWF and Unilever.

Summary info

RTRS: Initiation of consultation in 2004, first certification c. June 2011. Current price of certificates is USD5. 90,500 ha currently certified.

RSPO: Initiation of consultation in 2002, first certification c. end 2008. Current price of certificates is USD1. Over 1 million ha currently certified and 2.6 million ha promised in timebound plans by 2020.

Partial vs. full certification

RTRS: A producer can certify part of his production, but for his entire production area, he needs to implement some fundamental criteria e.g. not to deforest HCVA in non-certified areas. It is up to the producer to determine how much market demand there is for certified soy, so no specific percentage for certification is required (i.e. partial certification is OK).

RSPO: Since Nov 2008, growers have to timetable their adoption plans. Producers have to submit time-bound plans for their certification efforts; they are required to certify all their mills & supply bases (i.e. full / 100% certification is required). Clause 4.2.4 states: “A challenging time-bound plan for certifying all its relevant entities is submitted to the Certification Body (CB) during the first certification audit.” Source: “RSPO Certification Systems, Final document approved by RSPO Executive Board, 26 June 2007, Approved by Executive Board on 3 March 2011 on Revised clause 4.2.4.”

Principles & criteria

RTRS: 5 principles, 28 criteria, 95 indicators.

RSPO: 8 principles, 39 criteria, 118 indicators.

Phase-in compliance

RTRS: Gives producer 3 years to phase-in compliance. Allows partial compliance of 62% in year 1 and 86% in year 2, prior to 100% compliance in year 3.

RSPO: Phase-in not available.

HCV assessments

RTRS: Not required if expansion of soy cultivation is a) in line with an RTRS-approved map and system, or b) in non native forests areas and official land-use maps zone those areas for expansion or c) it is outside priority conservation areas.

RSPO: An HCV assessment, including stakeholder consultation, is conducted prior to any conversion. Also, refer to List of RSPO approved HCV assessors.

A quick glance indicates that on several fronts, RTRS is not as tough as RSPO. RTRS Standards also appears to better drafted, with a better categorisation of the P&C typology - this means fewer overlaps and confusions. When it comes time for RSPO to review its P&Cs (by 2012), it might look to the RTRS as an example.

Despite the more 'business-friendly' look of RTRS (vs. RSPO), Brazil soy association interests withdrew from RTRS. Brazil soy is slated to launch its own industry-led sustainability certification system, called "Soja Plus".

Subscribe to:

Posts (Atom)