For lack of a quorum, the RSPO GA will be rescheduled. Thus, we'll have to wait a while yet on the resolutions proposed. Khor Reports previewed them here, http://khorreports-palmoil.blogspot.com/2011/11/preview-of-rspo-8th-general-assembly.html.

"It was proposed at the meeting of November 24th 2011 that a process of obtaining votes electronically from non-attending members might be adopted, and the majority of members present in Sabah were in favour of this proposal. However, the Executive Board has since sought legal advice on the matter and now confirms that this proposal is not constitutional...."

http://www.rspo.org/?q=content/statement-executive-board-rspo-8th-general-assembly-ga8

This blog highlights news and views on markets, marketing, sustainability and political-economics of palm oil. Any views belong to the respective authors and do not represent that of any particular organization. I update this in my spare time. Since mid-2016, the more "comprehensive" news is available on customized request. Market news and big news continue to be updated. Thank you for reader interest that has generated over 130,000 page views in 2016.

Wednesday, December 7, 2011

Thursday, November 24, 2011

Preview of RSPO 8th General Assembly

We have been in Kota Kinabalu, Sabah, to attend the Roundtable for Sustainable Palm Oil's 9th Roundtable since Tuesday 22nd Nov. Today, the 8th General Assembly is being held. As such, we at Khor Reports thought to have a glance at what's coming up and point our readers to some pertinent links and information. Our comments in blue.

RSPO market updates on its website here, http://www.rspo.org/?q=node/2687. Do take a look for the latest figures. Looking forward, from about 5 million MT of certified product available, the submitted time-bound plans promise another 9 million MT. Thus, a total of 14 million MT will be available each year in a few years to come. On the buy-side, the just launched WWF Scorecard for palm oil buyers has found that 2015 demand for sustainable palm oil product is expected at 3.5 million MT each year. Depending on timing and new demand appearing, this suggests risk of some 11.5 million MT surplus supply. WWF did a study of buyers from Europe, Australia and Japan. RSPO is hoping to increase demand from key growing markets like China and India. It is also encouraging Dutch proposals that EU reduce import duties for sustainable palm oil vs non certified palm oil. EU by end 2014 will require labelling of all edible oils used on product packs i.e. the "vegetable oils" label will have to list out which oils were used. All these factors should help boost demand for sustainable products.

GreenPalm certificates pricing from its website here, http://www.greenpalm.org/. Price today is $1.59. It had fallen to US 50 cents and below in recent weeks. This compares to premium available from ISCC that ranges USD40-50, according to our contacts in the bio-fuels segment.

Resolution 6b: New Vision and Mission statements for the Roundtable on Sustainable Palm Oil; Executive Board of the Roundtable on Sustainable Palm Oil...... This is in answer to last year's MPOA / GAPKI resolution to review the "existing structure of the RSPO EB to reflect a better balance between the various stakeholders." The Executive Board / EB has reverted with a new Vision Statement for the RSPO which is: “RSPO will transform markets to make sustainable palm oil the norm”..... We are not sure precisely how the new Vision and Mission addresses the concern of MPOA / GAPKI that grower representation on the EB should be increased. Anyhow, GAPKI is no longer part of the RSPO. The Indonesian RSPO Growers Members now have a caucus, lead by Bapak Bambang Dwilaksono of First Resources, Bapak Edi Suhardi and Dr Gan Lian Tiong of Musim Mas, judging by the sign-offs on their resolutions. Indonesian grower interests have signed off on three resolutions, while Malaysian grower interests have only signed off on one. A MPOA representative was reported to suggest a halt in certification, but there has been no announcement or action by Malaysian companies on this suggestion.

Resolution 6c: Creation Of New Category Of Ordinary Membership For ‘Transnational Companies And Organisations’; Malaysian Palm Oil Association, FELDA, PT Musim Mas, Rabobank, HSBC Bank Malaysia Berhad, Unilever, and Growers from the Rest of the World...... This is also in answer to the MPOA / GAPKI resolution to review the "existing structure of the RSPO EB to reflect a better balance between the various stakeholders." The vertically integrated oil palm growers are seeking an additional seat on the EB. The big groups include Wilmar and Sime Darby.

Resolution 6d: Request for all RSPO Ordinary members to submit Time Bound Plans; The Zoological Society of London, WWF International, Conservation International,

Fauna and Flora International......This year, 66% of growers (Total no. members in category: 83), 43% of processors and traders (Total no. members in category: 146), 70% of consumer goods manufacturers (Total no. members in category: 105) and 76% of retailers (Total no. members in category: 25 members) have submitted annual progress reports to the RSPO1. Therefore, as many as 148 out of the 359 (41%) RSPO members in these categories did not submit a progress report.... This would require the members who are still in "wait and see" mode to have to act, and implement the RSPO P&Cs for their segment, across 100% of their production. RSPO is rather unusual in requiring 100% implementation. Other agricultural certification systems, like the Roundtable for Sustainable Soy, allow for partial certification (although for some key basic criteria, complete adherence is required).

Resolution 6e: Carry Forward of unsold certified sustainable palm products; Indonesian RSPO Growers Members......This reflects the grower's concern (and some frustration) at market offtake shortfalls for certified products. In recent months, this has stood at some 50%. A presentation by Kraft highlighted that this level of market off-take is quite "normal." In general, it would therefore seem that sustainability certification is generally more enthusiastically done by producers while buyers are more laid back about buying this. Perhaps the first group is keen to compete with each other for market access to the top buyers, and the buyers are more gradual and cautious, and keen to achieve sustainability with low or no premium? Whatever is the case, it looks like its a buyer's market in the food segment.

Resolution 6f: There is a need for a more balance representation in the RSPO Grievance Panel and a time-frame for closing of the complaints & grievances process.; Indonesian RSPO Growers Members......The composition of the core Grievance Panel is made up of the RSPO President (Unilever), environment (WWF Switzerland), social (Oxfam), producer (Malaysian Palm Oil Association) and the Affiliate Member (Dato’ Henry Barlow). Additional RSPO Ordinary or Affiliate Members may be called-upon to participate in the Grievance Panel as deemed appropriate by the core Grievance Panel......(The resolution proposes that ) The RSPO restructures the core members of Grievance Panel to include a representative from Indonesian Grower and that the RSPO reviews the grievance procedure to include a time-frame to close the case upon agreement by the alleged member to the recommended action of the Grievance Panel..... This likely reflects the rise of conflicts and frustration with the timing of dispute resolutions. Of late, social issues have become quite prominent, as evidenced by Oxfam's recent report on land grabbing (highlighting Sime Darby's Sanggau case) and several cases are also highlighted on the website of the Forest People's Programme (includes a complaint against Sime Darby in Liberia). A significant case is that of "IOI-Pelita," resulting in a halt to all certificate issuance to the IOI Group when they could not resolve the matter in 28 days. At the side-lines, we at Khor Reports hear that quite a few growers were busy in meetings with NGOs on various such cases. It would be good to have updates on the allegations and the cases, so as not cause unnecessary damage to reputations and to clarify the issues and how they were resolved (if found true).

Nominations for Executive Board elections for Category: Processors and Traders; Organisation : Olam International Ltd; Name of Nominee : Vasanth Subramaniam; Designation : Senior Vice President and Head of the Palm Business..... Olam is very fast-growing agricultural products supply-chain manager. It is moving aggressively upstream, into oil palm developments in Africa.

Self-nomination for candidate to the RSPO Executive Board, GA8 2011; Name of Organisation: Fauna & Flora International (FFI); Membership Category: Environment / Nature Conservation NGOs; Nominee: Darmawan Liswanto (Passport: Darmawan Lie); Designation: FFI Indonesia Country Programme Director......

RSPO Treasurer’s Report. Financial results for the year ended 30 June 2011. The RSPO group recorded a surplus of RM1,017,000 for the year ended 30 June 2011 (2010: RM2,253,000). Subscription income increased to RM3,975,000 from RM3,314,000 as membership numbers rose to 689 at 30 June 2011 (2010: 480). Income from sustainable palm oil trade rose to RM5,095,000 from RM2,822,000 the previous year, increasingly the main source of RSPO income. Operating costs increased as planned, to RM6,116,000 (2010: RM2,730,000)......

RSPO market updates on its website here, http://www.rspo.org/?q=node/2687. Do take a look for the latest figures. Looking forward, from about 5 million MT of certified product available, the submitted time-bound plans promise another 9 million MT. Thus, a total of 14 million MT will be available each year in a few years to come. On the buy-side, the just launched WWF Scorecard for palm oil buyers has found that 2015 demand for sustainable palm oil product is expected at 3.5 million MT each year. Depending on timing and new demand appearing, this suggests risk of some 11.5 million MT surplus supply. WWF did a study of buyers from Europe, Australia and Japan. RSPO is hoping to increase demand from key growing markets like China and India. It is also encouraging Dutch proposals that EU reduce import duties for sustainable palm oil vs non certified palm oil. EU by end 2014 will require labelling of all edible oils used on product packs i.e. the "vegetable oils" label will have to list out which oils were used. All these factors should help boost demand for sustainable products.

GreenPalm certificates pricing from its website here, http://www.greenpalm.org/. Price today is $1.59. It had fallen to US 50 cents and below in recent weeks. This compares to premium available from ISCC that ranges USD40-50, according to our contacts in the bio-fuels segment.

Resolution 6b: New Vision and Mission statements for the Roundtable on Sustainable Palm Oil; Executive Board of the Roundtable on Sustainable Palm Oil...... This is in answer to last year's MPOA / GAPKI resolution to review the "existing structure of the RSPO EB to reflect a better balance between the various stakeholders." The Executive Board / EB has reverted with a new Vision Statement for the RSPO which is: “RSPO will transform markets to make sustainable palm oil the norm”..... We are not sure precisely how the new Vision and Mission addresses the concern of MPOA / GAPKI that grower representation on the EB should be increased. Anyhow, GAPKI is no longer part of the RSPO. The Indonesian RSPO Growers Members now have a caucus, lead by Bapak Bambang Dwilaksono of First Resources, Bapak Edi Suhardi and Dr Gan Lian Tiong of Musim Mas, judging by the sign-offs on their resolutions. Indonesian grower interests have signed off on three resolutions, while Malaysian grower interests have only signed off on one. A MPOA representative was reported to suggest a halt in certification, but there has been no announcement or action by Malaysian companies on this suggestion.

Resolution 6c: Creation Of New Category Of Ordinary Membership For ‘Transnational Companies And Organisations’; Malaysian Palm Oil Association, FELDA, PT Musim Mas, Rabobank, HSBC Bank Malaysia Berhad, Unilever, and Growers from the Rest of the World...... This is also in answer to the MPOA / GAPKI resolution to review the "existing structure of the RSPO EB to reflect a better balance between the various stakeholders." The vertically integrated oil palm growers are seeking an additional seat on the EB. The big groups include Wilmar and Sime Darby.

Resolution 6d: Request for all RSPO Ordinary members to submit Time Bound Plans; The Zoological Society of London, WWF International, Conservation International,

Fauna and Flora International......This year, 66% of growers (Total no. members in category: 83), 43% of processors and traders (Total no. members in category: 146), 70% of consumer goods manufacturers (Total no. members in category: 105) and 76% of retailers (Total no. members in category: 25 members) have submitted annual progress reports to the RSPO1. Therefore, as many as 148 out of the 359 (41%) RSPO members in these categories did not submit a progress report.... This would require the members who are still in "wait and see" mode to have to act, and implement the RSPO P&Cs for their segment, across 100% of their production. RSPO is rather unusual in requiring 100% implementation. Other agricultural certification systems, like the Roundtable for Sustainable Soy, allow for partial certification (although for some key basic criteria, complete adherence is required).

Resolution 6e: Carry Forward of unsold certified sustainable palm products; Indonesian RSPO Growers Members......This reflects the grower's concern (and some frustration) at market offtake shortfalls for certified products. In recent months, this has stood at some 50%. A presentation by Kraft highlighted that this level of market off-take is quite "normal." In general, it would therefore seem that sustainability certification is generally more enthusiastically done by producers while buyers are more laid back about buying this. Perhaps the first group is keen to compete with each other for market access to the top buyers, and the buyers are more gradual and cautious, and keen to achieve sustainability with low or no premium? Whatever is the case, it looks like its a buyer's market in the food segment.

Resolution 6f: There is a need for a more balance representation in the RSPO Grievance Panel and a time-frame for closing of the complaints & grievances process.; Indonesian RSPO Growers Members......The composition of the core Grievance Panel is made up of the RSPO President (Unilever), environment (WWF Switzerland), social (Oxfam), producer (Malaysian Palm Oil Association) and the Affiliate Member (Dato’ Henry Barlow). Additional RSPO Ordinary or Affiliate Members may be called-upon to participate in the Grievance Panel as deemed appropriate by the core Grievance Panel......(The resolution proposes that ) The RSPO restructures the core members of Grievance Panel to include a representative from Indonesian Grower and that the RSPO reviews the grievance procedure to include a time-frame to close the case upon agreement by the alleged member to the recommended action of the Grievance Panel..... This likely reflects the rise of conflicts and frustration with the timing of dispute resolutions. Of late, social issues have become quite prominent, as evidenced by Oxfam's recent report on land grabbing (highlighting Sime Darby's Sanggau case) and several cases are also highlighted on the website of the Forest People's Programme (includes a complaint against Sime Darby in Liberia). A significant case is that of "IOI-Pelita," resulting in a halt to all certificate issuance to the IOI Group when they could not resolve the matter in 28 days. At the side-lines, we at Khor Reports hear that quite a few growers were busy in meetings with NGOs on various such cases. It would be good to have updates on the allegations and the cases, so as not cause unnecessary damage to reputations and to clarify the issues and how they were resolved (if found true).

Nominations for Executive Board elections for Category: Processors and Traders; Organisation : Olam International Ltd; Name of Nominee : Vasanth Subramaniam; Designation : Senior Vice President and Head of the Palm Business..... Olam is very fast-growing agricultural products supply-chain manager. It is moving aggressively upstream, into oil palm developments in Africa.

Self-nomination for candidate to the RSPO Executive Board, GA8 2011; Name of Organisation: Fauna & Flora International (FFI); Membership Category: Environment / Nature Conservation NGOs; Nominee: Darmawan Liswanto (Passport: Darmawan Lie); Designation: FFI Indonesia Country Programme Director......

RSPO Treasurer’s Report. Financial results for the year ended 30 June 2011. The RSPO group recorded a surplus of RM1,017,000 for the year ended 30 June 2011 (2010: RM2,253,000). Subscription income increased to RM3,975,000 from RM3,314,000 as membership numbers rose to 689 at 30 June 2011 (2010: 480). Income from sustainable palm oil trade rose to RM5,095,000 from RM2,822,000 the previous year, increasingly the main source of RSPO income. Operating costs increased as planned, to RM6,116,000 (2010: RM2,730,000)......

Friday, October 21, 2011

RSPO farmers and facilitators - who earns what?

We, at Khor Reports, recently attended a conference in Singapore that was largely concerned with deforestation in SE Asia. It was a well attended event, with representatives from the Norway and Indonesia governments, a video from the UN's forest secretariat and a strong presence from key environmental NGOs, a few with 100-year histories (information about the conference here: http://web1.iseas.edu.sg/?p=4977). The latter presented some information about their REDD+ projects. These seek to bring other incomes to local peoples, to give them an alternative to agriculture extensification i.e. cutting down trees and planting crops such as palm oil.

Market perversion, with 10-20% to local peoples / farmers

A crucial question from the audience was left unanswered in the public forum. A professor asked how much money actually goes to the local community and how much to bankers, consultants and other facilitators (I paraphrase). We all, should be concerned about how much in the $1 goes to the different parties involved in sustainability efforts.

So, let's take a look at the Roundtable for Sustainable Palm Oil's (RSPO) Certified Sustainable Palm Oil (CSPO) at GreenPalm (the book and claim system). At present, the price for CSPO certificates is US 25 cents (down from USD40 or so), and the brokerage fee is USD1.50 and the fee to the RSPO is USD1.00 (source:http://www.greenpalm.org/en/faqs/general#how-much-are-brokerage-fees). Thus, a buyer of 1 mt of this sustainable palm oil would pay a premium of USD2.75. In effect, 9% of the premium goes to the planter of palm oil and 91% goes to the facilitators (GreenPalm and the RSPO)#.

This is the opposite of what we would expect. We all would like to see the bulk being earned by the local peoples / farmers i.e. the 'doers'. In reality, the opposite is the case. Thus, it is a perversion of the so-called market (MS Word's thesaurus likens 'perversion' to the words parody, caricature, distortion, falsification, twisting, slanting...).

Is the current RSPO GreenPalm situation uncommon? Unfortunately, it seems to be consistent with the feedback that various sustainability efforts may only pay 10-20 cents in the dollar to the local doers / peoples. Perhaps a key problem is the collapse of voluntary market prices for many types of sustainability credits and certificates (and the outlook isn't good, given the economic troubles ailing the developed world). Other problems could be sub-optimal structuring of the projects and that too many parties are involved, with each seeking some upfront and fixed payment that is not tied to the price and performance of the traded certificate.

Good practices - 3 lessons from the NGO sector

We should ask this: what is good practice? Let's learn from the NGOs. They are often judged by the amount that they spend on their projects vs. what they spend on administration and fund raising. A common target threshold is some 85 cents in the dollar going to project or program work.

Take a look at Oxfam Hong Kong's 'Use of Donations' statement here, http://www.oxfam.org.hk/en/useofdonations.aspx. Another good practice for NGOs is the local sourcing of funding with low / no reliance on overseas HQ and government funding. This vastly improves a charity's autonomy. Along this vein, Khor Reports ventures to suggest more good practices: a wide breadth of funding, especially from individuals and less from corporates, and with 'limits' on single-source funding to avoid 'capture' by particular interests. Oxfam also says that for emergency efforts, "ALL donations – exactly 100% – go to assist people in need."

Thus, the palm oil sector could draw three (3) lessons for its sustainability programs: i) target no more than 15% on facilitation costs, ii) aim to localize and be autonomous, while avoiding capture by special interests and iii) for special worthy cases e.g. independent smallholders, zero facilitation costs.

Fix it

Thus, NGOs offer lessons in good practices. Clearly, NGOs should replicate such practices when designing and implementing projects affecting local peoples in developing countries. We hope to see that most of their programs deliver 85% benefits to the local peoples / farmers. These are the people nearer the bottom of the 99% that the Occupy Wall Street demonstrators are telling the 1% (the rich) not to forget. They say "the system is broke," and we at Khor Reports recognise in this statement, two meanings of the word "broke". So, let's not have socio-environmental efforts become another financial tool of (or captured by) rich interests. Let's fix it.

#In this, we have not even considered the direct and indirect costs of certification (the former estimated at USD6-12 per mt for corporate planters).

Market perversion, with 10-20% to local peoples / farmers

A crucial question from the audience was left unanswered in the public forum. A professor asked how much money actually goes to the local community and how much to bankers, consultants and other facilitators (I paraphrase). We all, should be concerned about how much in the $1 goes to the different parties involved in sustainability efforts.

So, let's take a look at the Roundtable for Sustainable Palm Oil's (RSPO) Certified Sustainable Palm Oil (CSPO) at GreenPalm (the book and claim system). At present, the price for CSPO certificates is US 25 cents (down from USD40 or so), and the brokerage fee is USD1.50 and the fee to the RSPO is USD1.00 (source:http://www.greenpalm.org/en/faqs/general#how-much-are-brokerage-fees). Thus, a buyer of 1 mt of this sustainable palm oil would pay a premium of USD2.75. In effect, 9% of the premium goes to the planter of palm oil and 91% goes to the facilitators (GreenPalm and the RSPO)#.

This is the opposite of what we would expect. We all would like to see the bulk being earned by the local peoples / farmers i.e. the 'doers'. In reality, the opposite is the case. Thus, it is a perversion of the so-called market (MS Word's thesaurus likens 'perversion' to the words parody, caricature, distortion, falsification, twisting, slanting...).

Is the current RSPO GreenPalm situation uncommon? Unfortunately, it seems to be consistent with the feedback that various sustainability efforts may only pay 10-20 cents in the dollar to the local doers / peoples. Perhaps a key problem is the collapse of voluntary market prices for many types of sustainability credits and certificates (and the outlook isn't good, given the economic troubles ailing the developed world). Other problems could be sub-optimal structuring of the projects and that too many parties are involved, with each seeking some upfront and fixed payment that is not tied to the price and performance of the traded certificate.

Good practices - 3 lessons from the NGO sector

We should ask this: what is good practice? Let's learn from the NGOs. They are often judged by the amount that they spend on their projects vs. what they spend on administration and fund raising. A common target threshold is some 85 cents in the dollar going to project or program work.

Take a look at Oxfam Hong Kong's 'Use of Donations' statement here, http://www.oxfam.org.hk/en/useofdonations.aspx. Another good practice for NGOs is the local sourcing of funding with low / no reliance on overseas HQ and government funding. This vastly improves a charity's autonomy. Along this vein, Khor Reports ventures to suggest more good practices: a wide breadth of funding, especially from individuals and less from corporates, and with 'limits' on single-source funding to avoid 'capture' by particular interests. Oxfam also says that for emergency efforts, "ALL donations – exactly 100% – go to assist people in need."

Thus, the palm oil sector could draw three (3) lessons for its sustainability programs: i) target no more than 15% on facilitation costs, ii) aim to localize and be autonomous, while avoiding capture by special interests and iii) for special worthy cases e.g. independent smallholders, zero facilitation costs.

Fix it

Thus, NGOs offer lessons in good practices. Clearly, NGOs should replicate such practices when designing and implementing projects affecting local peoples in developing countries. We hope to see that most of their programs deliver 85% benefits to the local peoples / farmers. These are the people nearer the bottom of the 99% that the Occupy Wall Street demonstrators are telling the 1% (the rich) not to forget. They say "the system is broke," and we at Khor Reports recognise in this statement, two meanings of the word "broke". So, let's not have socio-environmental efforts become another financial tool of (or captured by) rich interests. Let's fix it.

#In this, we have not even considered the direct and indirect costs of certification (the former estimated at USD6-12 per mt for corporate planters).

Wednesday, October 12, 2011

Palm oil on fast-track vs. others

The Star reports, October 11, 2011, "Demand for certified sustainable palm oil surges 70%":

RSPO president Jan Kees Vis said in a statement that “the current number sparks hopes that a breakthrough is near.”“Historically, there has always been a delay in market take-up versus production increase, as buyers of large companies have to commit as long as a year in advance to buy raw materials,” he said. “They will only sign on to what they are sure they can actually purchase from the market in the future,” he added. Secretary-general Darrel Webber also noted that “a significant number of retailers, consumer goods manufacturers, processors and traders have committed to 100% CSPO by 2015.”..........

Khor Reports comment:

a) The increase in market off-take to 70% from its recent plateau at 50% will surely be welcomed by producers of CSPO. Perhaps buyers have been reacting to the recent flap at RSPO: the withdrawal of GAPKI and the call associated with MPOA for a 3-year moratorium on certification (but with no corporate reactions yet).

b) Sometime ago, Unilever said that they accounted for some 50% of CSPO purchases. As the lead product manufacturer in RSPO, perhaps Unilever stepped up its buying recently? This company is one of the key drivers of the agriculture sustainability sourcing via the WWF-driven 'roundtables schemes'.

c) Let's take a quick look at Unilever's commitments on sourcing sustainable inputs. The graphic below shows that palm oil is on the fast-track with a 'by 2015' target, while other competing oils will be sustainably sourced only by 2020. Moreover, news reports say that Unilever seeks to replace palm oil in its Dove soap and lotions within a few years. In this regard, palm oil has been selected as the oil most in urgent need of sustainable requirements (and some replacement).

d) The palm oil fast-track by buyers has only been exceeded by the fast-track that growers have taken in providing RSPO CSPO to the market. With the recent sharp rise in CSPO, it appears that palm oil is some 7-9 years ahead of its competitor oils - soybean oil, rapeseed oil and sunflower oil.

e) This assumes that many manufacturers also use Unilever's timeframe and that the other oil growers take a more moderate approach e.g. the more business-friendly RTRS / soy roundtable allows for partial certification while RSPO requires rapid or 'challenging' timeframe for 100% certification.

RSPO president Jan Kees Vis said in a statement that “the current number sparks hopes that a breakthrough is near.”“Historically, there has always been a delay in market take-up versus production increase, as buyers of large companies have to commit as long as a year in advance to buy raw materials,” he said. “They will only sign on to what they are sure they can actually purchase from the market in the future,” he added. Secretary-general Darrel Webber also noted that “a significant number of retailers, consumer goods manufacturers, processors and traders have committed to 100% CSPO by 2015.”..........

Khor Reports comment:

a) The increase in market off-take to 70% from its recent plateau at 50% will surely be welcomed by producers of CSPO. Perhaps buyers have been reacting to the recent flap at RSPO: the withdrawal of GAPKI and the call associated with MPOA for a 3-year moratorium on certification (but with no corporate reactions yet).

b) Sometime ago, Unilever said that they accounted for some 50% of CSPO purchases. As the lead product manufacturer in RSPO, perhaps Unilever stepped up its buying recently? This company is one of the key drivers of the agriculture sustainability sourcing via the WWF-driven 'roundtables schemes'.

c) Let's take a quick look at Unilever's commitments on sourcing sustainable inputs. The graphic below shows that palm oil is on the fast-track with a 'by 2015' target, while other competing oils will be sustainably sourced only by 2020. Moreover, news reports say that Unilever seeks to replace palm oil in its Dove soap and lotions within a few years. In this regard, palm oil has been selected as the oil most in urgent need of sustainable requirements (and some replacement).

d) The palm oil fast-track by buyers has only been exceeded by the fast-track that growers have taken in providing RSPO CSPO to the market. With the recent sharp rise in CSPO, it appears that palm oil is some 7-9 years ahead of its competitor oils - soybean oil, rapeseed oil and sunflower oil.

e) This assumes that many manufacturers also use Unilever's timeframe and that the other oil growers take a more moderate approach e.g. the more business-friendly RTRS / soy roundtable allows for partial certification while RSPO requires rapid or 'challenging' timeframe for 100% certification.

Friday, October 7, 2011

MPOA calls for halt to new RSPO certification?

“We want to see the current RSPO certified palm oil production of 5.1 million tonnes be fully taken up by Western buyers,” said MPOA vice-chairman Boon Weng Siew. Of the total RSPO-certified palm production, MPOA claimed that only 40% was taken up while the CSPO premium had plunged to only 30 US cents compared with US$50 per tonne in 2008.... Bek-Nielsen...said the world palm oil producers must unite and stressed that “We should not certify any new production units unless demand matches the supply of CSPO. It is time for the end-users to live up to their rethorics.”... An industry member of MPOA said the association might seek for a three-year moratorium to stop Malaysian planters from pursuing their on-going RSPO certification at the RSPO 9th Annual Meeting Roundtable in Sabah next month....“We will strongly push for this agenda,” he said. This is in view of the pledges given by Western food and consumer goods to use only CSPO in their operations by 2015.... reports The Star, 6 Oct 2011, "Malaysian Palm Oil Association won’t quit Roundtable on Sustainable Palm Oil," http://biz.thestar.com.my/news/story.asp?file=/2011/10/6/business/9638574&sec=business.

Khor Reports comment: Hot on the heels of last week's pullout from RSPO by GAPKI, Malaysia's key producer association affirms its membership, but calls for a halt to new certification. There has been a small glut in RSPO CSPO or certified sustainable palm oil, as the enthusiasm of producers for this sustainable product has not yet been met by sufficient buyer interest. Last year, we at Khor Reports speculated in our newsletter #2 that producers might seek to clear the overhang, but we had no idea then what might be the mechanism (download our report and refer to page 6, Option E: https://sites.google.com/site/khorreports2011/palmoil_strat_analysis/khorreport002-palm_oil-rspo_growers-100826.pdf?attredirects=0&d=1). It will be interesting to look out for corporate reactions to the recent moves by GAPKI and MPOA.

For more background, please refer to other postings in this blog, and Khor Yu Leng's article in Lipid Technology, "The oil palm industry bows to NGO campaigns," May 2011, http://onlinelibrary.wiley.com/doi/10.1002/lite.201100106/abstract.

Khor Yu Leng was interviewed for today's The Edge Daily: "Independent agribusiness analyst Khor Yu Leng, who has tracked sustainability certification practises, says oil palm players cannot be blamed for wanting a more level playing field with other types of vegetable oil producers. “RTRS, the standard for sustainable soybean, is more business friendly versus the RSPO, despite their being sister organizations,” she said. She thinks the palm players will move towards having more than one type of certification, to meet different market needs."

Khor Reports comment: Hot on the heels of last week's pullout from RSPO by GAPKI, Malaysia's key producer association affirms its membership, but calls for a halt to new certification. There has been a small glut in RSPO CSPO or certified sustainable palm oil, as the enthusiasm of producers for this sustainable product has not yet been met by sufficient buyer interest. Last year, we at Khor Reports speculated in our newsletter #2 that producers might seek to clear the overhang, but we had no idea then what might be the mechanism (download our report and refer to page 6, Option E: https://sites.google.com/site/khorreports2011/palmoil_strat_analysis/khorreport002-palm_oil-rspo_growers-100826.pdf?attredirects=0&d=1). It will be interesting to look out for corporate reactions to the recent moves by GAPKI and MPOA.

For more background, please refer to other postings in this blog, and Khor Yu Leng's article in Lipid Technology, "The oil palm industry bows to NGO campaigns," May 2011, http://onlinelibrary.wiley.com/doi/10.1002/lite.201100106/abstract.

Khor Yu Leng was interviewed for today's The Edge Daily: "Independent agribusiness analyst Khor Yu Leng, who has tracked sustainability certification practises, says oil palm players cannot be blamed for wanting a more level playing field with other types of vegetable oil producers. “RTRS, the standard for sustainable soybean, is more business friendly versus the RSPO, despite their being sister organizations,” she said. She thinks the palm players will move towards having more than one type of certification, to meet different market needs."

Felda listing mooted again

Two articles on Felda in the print and online news today.

a) Felda commercial arm to list? It will create world’s largest listed plantation firm, http://biz.thestar.com.my/news/story.asp?file=/2011/10/7/business/9648450&sec=business

b) Concerns at Felda's Coop, http://www.malaysia-chronicle.com/index.php?option=com_k2&view=item&id=20674:isa-samad-makes-his-move-but-felda-settlers-call-for-his-removal-as-co-op-chief&Itemid=2

Khor Reports comment: Rumours of the listing of Felda Group or one of its key entities have recurred over the years. The Group, controls some 850,000 Ha of both settler and commercial land bank. For a long time, it has been the largest plantation in SE Asia, if not the world (if one excludes the fluctuating figure of the unplanted reserves of the likes of Sime Darby and Golden Agri). It grew out of a land resettlement scheme, under the Federal Land Development Authority. What has held up a listing of a Felda unit for decades? After all, Malaysia is well known for privatizations and public-listings of government-linked entities. The key issue is this: majority ownership is held Koperasi Permodalan Felda or KPF (website: http://kpf.felda.net.my/Pages/kpf.aspx). Under a cooperative, key corporate actions would require that settlers and staff of Felda (current and former?) who are members of KPF, would have to vote on it, on the "one man, one vote" basis.

Interviewed by The Edge in January 2011, "Taking Felda to the next level,"

http://www.feldaholdings.com/content.php?h=4177&lang=EN.

a) Felda commercial arm to list? It will create world’s largest listed plantation firm, http://biz.thestar.com.my/news/story.asp?file=/2011/10/7/business/9648450&sec=business

b) Concerns at Felda's Coop, http://www.malaysia-chronicle.com/index.php?option=com_k2&view=item&id=20674:isa-samad-makes-his-move-but-felda-settlers-call-for-his-removal-as-co-op-chief&Itemid=2

Khor Reports comment: Rumours of the listing of Felda Group or one of its key entities have recurred over the years. The Group, controls some 850,000 Ha of both settler and commercial land bank. For a long time, it has been the largest plantation in SE Asia, if not the world (if one excludes the fluctuating figure of the unplanted reserves of the likes of Sime Darby and Golden Agri). It grew out of a land resettlement scheme, under the Federal Land Development Authority. What has held up a listing of a Felda unit for decades? After all, Malaysia is well known for privatizations and public-listings of government-linked entities. The key issue is this: majority ownership is held Koperasi Permodalan Felda or KPF (website: http://kpf.felda.net.my/Pages/kpf.aspx). Under a cooperative, key corporate actions would require that settlers and staff of Felda (current and former?) who are members of KPF, would have to vote on it, on the "one man, one vote" basis.

Interviewed by The Edge in January 2011, "Taking Felda to the next level,"

http://www.feldaholdings.com/content.php?h=4177&lang=EN.

Monday, October 3, 2011

RSPO vs. soy roundtable

News: GAPKI, the key palm oil producer association of Indonesia withdraws from its membership and its Executive Board role in the RSPO. Source: http://www.rspo.org/?q=content/statement-gapki%E2%80%99s-withdrawal-rspo.

Khor Reports comment: There had been market rumours. Also, the growers' collective dissatisfaction with RSPO is well known. But, seeing is believing. It has happened; Indonesia is following the play book that Brazil has also used. Read about it here in our Khor Reports, Palm Oil Strategic Analysis newsletter #2: https://sites.google.com/site/khorreports2011/palmoil_strat_analysis/khorreport002-palm_oil-rspo_growers-100826.pdf?attredirects=0&d=1.

Since the subject of soy crops up, let's do a quick comparison of some of the key features and achievements of RSPO and its sister organisation in the soy sector, the Roundtable for Responsible Soy (RTRS). RSPO and RTRS have some common Executive Board members - including WWF and Unilever.

Summary info

RTRS: Initiation of consultation in 2004, first certification c. June 2011. Current price of certificates is USD5. 90,500 ha currently certified.

RSPO: Initiation of consultation in 2002, first certification c. end 2008. Current price of certificates is USD1. Over 1 million ha currently certified and 2.6 million ha promised in timebound plans by 2020.

Partial vs. full certification

RTRS: A producer can certify part of his production, but for his entire production area, he needs to implement some fundamental criteria e.g. not to deforest HCVA in non-certified areas. It is up to the producer to determine how much market demand there is for certified soy, so no specific percentage for certification is required (i.e. partial certification is OK).

RSPO: Since Nov 2008, growers have to timetable their adoption plans. Producers have to submit time-bound plans for their certification efforts; they are required to certify all their mills & supply bases (i.e. full / 100% certification is required). Clause 4.2.4 states: “A challenging time-bound plan for certifying all its relevant entities is submitted to the Certification Body (CB) during the first certification audit.” Source: “RSPO Certification Systems, Final document approved by RSPO Executive Board, 26 June 2007, Approved by Executive Board on 3 March 2011 on Revised clause 4.2.4.”

Principles & criteria

RTRS: 5 principles, 28 criteria, 95 indicators.

RSPO: 8 principles, 39 criteria, 118 indicators.

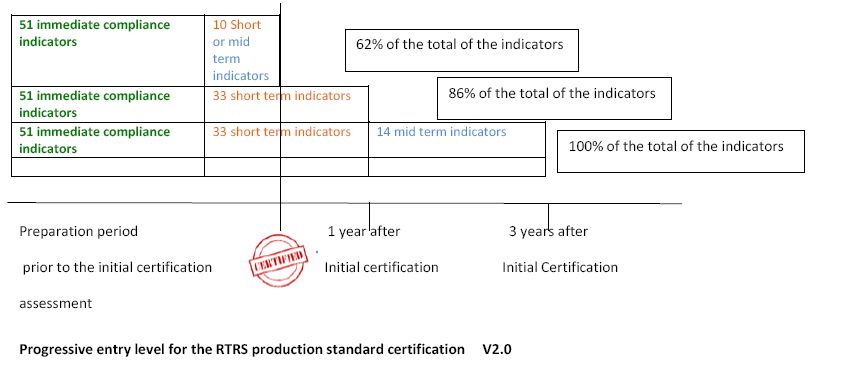

Phase-in compliance

RTRS: Gives producer 3 years to phase-in compliance. Allows partial compliance of 62% in year 1 and 86% in year 2, prior to 100% compliance in year 3.

RSPO: Phase-in not available.

HCV assessments

RTRS: Not required if expansion of soy cultivation is a) in line with an RTRS-approved map and system, or b) in non native forests areas and official land-use maps zone those areas for expansion or c) it is outside priority conservation areas.

RSPO: An HCV assessment, including stakeholder consultation, is conducted prior to any conversion. Also, refer to List of RSPO approved HCV assessors.

A quick glance indicates that on several fronts, RTRS is not as tough as RSPO. RTRS Standards also appears to better drafted, with a better categorisation of the P&C typology - this means fewer overlaps and confusions. When it comes time for RSPO to review its P&Cs (by 2012), it might look to the RTRS as an example.

Despite the more 'business-friendly' look of RTRS (vs. RSPO), Brazil soy association interests withdrew from RTRS. Brazil soy is slated to launch its own industry-led sustainability certification system, called "Soja Plus".

Khor Reports comment: There had been market rumours. Also, the growers' collective dissatisfaction with RSPO is well known. But, seeing is believing. It has happened; Indonesia is following the play book that Brazil has also used. Read about it here in our Khor Reports, Palm Oil Strategic Analysis newsletter #2: https://sites.google.com/site/khorreports2011/palmoil_strat_analysis/khorreport002-palm_oil-rspo_growers-100826.pdf?attredirects=0&d=1.

Since the subject of soy crops up, let's do a quick comparison of some of the key features and achievements of RSPO and its sister organisation in the soy sector, the Roundtable for Responsible Soy (RTRS). RSPO and RTRS have some common Executive Board members - including WWF and Unilever.

Summary info

RTRS: Initiation of consultation in 2004, first certification c. June 2011. Current price of certificates is USD5. 90,500 ha currently certified.

RSPO: Initiation of consultation in 2002, first certification c. end 2008. Current price of certificates is USD1. Over 1 million ha currently certified and 2.6 million ha promised in timebound plans by 2020.

Partial vs. full certification

RTRS: A producer can certify part of his production, but for his entire production area, he needs to implement some fundamental criteria e.g. not to deforest HCVA in non-certified areas. It is up to the producer to determine how much market demand there is for certified soy, so no specific percentage for certification is required (i.e. partial certification is OK).

RSPO: Since Nov 2008, growers have to timetable their adoption plans. Producers have to submit time-bound plans for their certification efforts; they are required to certify all their mills & supply bases (i.e. full / 100% certification is required). Clause 4.2.4 states: “A challenging time-bound plan for certifying all its relevant entities is submitted to the Certification Body (CB) during the first certification audit.” Source: “RSPO Certification Systems, Final document approved by RSPO Executive Board, 26 June 2007, Approved by Executive Board on 3 March 2011 on Revised clause 4.2.4.”

Principles & criteria

RTRS: 5 principles, 28 criteria, 95 indicators.

RSPO: 8 principles, 39 criteria, 118 indicators.

Phase-in compliance

RTRS: Gives producer 3 years to phase-in compliance. Allows partial compliance of 62% in year 1 and 86% in year 2, prior to 100% compliance in year 3.

RSPO: Phase-in not available.

HCV assessments

RTRS: Not required if expansion of soy cultivation is a) in line with an RTRS-approved map and system, or b) in non native forests areas and official land-use maps zone those areas for expansion or c) it is outside priority conservation areas.

RSPO: An HCV assessment, including stakeholder consultation, is conducted prior to any conversion. Also, refer to List of RSPO approved HCV assessors.

A quick glance indicates that on several fronts, RTRS is not as tough as RSPO. RTRS Standards also appears to better drafted, with a better categorisation of the P&C typology - this means fewer overlaps and confusions. When it comes time for RSPO to review its P&Cs (by 2012), it might look to the RTRS as an example.

Despite the more 'business-friendly' look of RTRS (vs. RSPO), Brazil soy association interests withdrew from RTRS. Brazil soy is slated to launch its own industry-led sustainability certification system, called "Soja Plus".

Monday, September 26, 2011

IFC / World Bank Group support of RSPO

IFC (part of the World Bank Group) supports the development of the RSPO, primarily through its Biodiversity and Agricultural Commodities program (BACP). Read about it via its flyer here, http://www.ifc.org/ifcext/sustainability.nsf/AttachmentsByTitle/fly_Biodiversity_BACP/$FILE/BACP+Flyer.pdf.

Reported in the BACP newsletter, Issue 10, June 2011:

Through its grant-making facility, BACP supports the RSPO both directly and indirectly.

BACP provided a grant directly to the RSPO to support a Biodiversity Coordinator and activities of the Biodiversity Technical Committee (BTC).

BACP has given grants to various NGOs and other organisations, in support of their efforts at RSPO, these include:

• PanEco Foundation is working to demonstrate the potential for palm oil production on Indonesia's 4.7 million hectares of degraded land in an effort to preserve the country’s biodiversity-rich areas of High Conservation Value (HCV) from being converted to palm oil plantations......

• The Zoological Society of London (ZSL) is working to 1. improve the effectiveness of the biodiversity-related RSPO Principles and Criteria......

• Fauna and Flora International (FFI) has been piloting an innovative partnership model that helps producer companies comply with the biodiversity-related criterion of the Roundtable for Sustainable Palm Oil (RSPO)’s Principles and Criteria. The partnership engages large-scale producers to take an active role in protecting and managing HCV areas on or adjacent to their concessions......

• The World Resources Institute (WRI) is working to make compliance with RSPO biodiversity related principles and criteria easier for producers by providing necessary information and toolkits for successful and sustainable production on degraded land......

IFC’s BACP also has various efforts Supporting the Round Table for Responsible Soy (RTRS).

BACP states: Agricultural expansion is the leading cause of habitat loss around the world and poses one of the gravest threats to global biodiversity. Tropical export commodities have dramatically increased production in the last fifty years, resulting in the destruction of much tropical habitat. The Biodiversity and Agricultural Commodities Program (BACP) seeks to reduce the threats posed by agriculture to biodiversity of global significance by transforming markets for target agricultural commodities. To transform the commodity markets, BACP supports projects that generate greater supply, demand and financing of biodiversity-friendly products. Projects must meet specific criteria and address one of the four following components:

1. Removing policy barriers

2. Supporting better production

3. Increasing demand for biodiversity-friendly products

4. Encouraging financial services to support biodiversity-friendly practices

Source: http://www.ifc.org/ifcext/sustainability.nsf/AttachmentsByTitle/newsletter_biodiversity_BACP_issue10/$FILE/BACP_Newsletter_Issue+10.pdf.

Khor Reports comment: NGOs and other organisations have been quick to avail themselves of BACP funding for their projects. It is surprising to us that growers (especially the smaller estates, smallholders and/or those operating near high conservation / sensitive areas), who may have quite a lot work to do too, do not seem to have done so yet (not listed among 'grantee highlights' in the BACP newsletter). Perhaps BACP could assist them too?

Reported in the BACP newsletter, Issue 10, June 2011:

Through its grant-making facility, BACP supports the RSPO both directly and indirectly.

BACP provided a grant directly to the RSPO to support a Biodiversity Coordinator and activities of the Biodiversity Technical Committee (BTC).

BACP has given grants to various NGOs and other organisations, in support of their efforts at RSPO, these include:

• PanEco Foundation is working to demonstrate the potential for palm oil production on Indonesia's 4.7 million hectares of degraded land in an effort to preserve the country’s biodiversity-rich areas of High Conservation Value (HCV) from being converted to palm oil plantations......

• The Zoological Society of London (ZSL) is working to 1. improve the effectiveness of the biodiversity-related RSPO Principles and Criteria......

• Fauna and Flora International (FFI) has been piloting an innovative partnership model that helps producer companies comply with the biodiversity-related criterion of the Roundtable for Sustainable Palm Oil (RSPO)’s Principles and Criteria. The partnership engages large-scale producers to take an active role in protecting and managing HCV areas on or adjacent to their concessions......

• The World Resources Institute (WRI) is working to make compliance with RSPO biodiversity related principles and criteria easier for producers by providing necessary information and toolkits for successful and sustainable production on degraded land......

IFC’s BACP also has various efforts Supporting the Round Table for Responsible Soy (RTRS).

BACP states: Agricultural expansion is the leading cause of habitat loss around the world and poses one of the gravest threats to global biodiversity. Tropical export commodities have dramatically increased production in the last fifty years, resulting in the destruction of much tropical habitat. The Biodiversity and Agricultural Commodities Program (BACP) seeks to reduce the threats posed by agriculture to biodiversity of global significance by transforming markets for target agricultural commodities. To transform the commodity markets, BACP supports projects that generate greater supply, demand and financing of biodiversity-friendly products. Projects must meet specific criteria and address one of the four following components:

1. Removing policy barriers

2. Supporting better production

3. Increasing demand for biodiversity-friendly products

4. Encouraging financial services to support biodiversity-friendly practices

Source: http://www.ifc.org/ifcext/sustainability.nsf/AttachmentsByTitle/newsletter_biodiversity_BACP_issue10/$FILE/BACP_Newsletter_Issue+10.pdf.

Khor Reports comment: NGOs and other organisations have been quick to avail themselves of BACP funding for their projects. It is surprising to us that growers (especially the smaller estates, smallholders and/or those operating near high conservation / sensitive areas), who may have quite a lot work to do too, do not seem to have done so yet (not listed among 'grantee highlights' in the BACP newsletter). Perhaps BACP could assist them too?

Tuesday, September 6, 2011

Greenpalm CSPO premium dives to 30 cents

Greenpalm reports on its website: "GreenPalm passes key milestone as 2 millionth certificate traded... GreenPalm, the certificate trading programme that enables businesses to support sustainable palm oil production, is celebrating the trade of its 2 millionth certificate. This milestone has been achieved in just over two and a half years, enabling palm oil producers to earn over $15m of additional income for operating sustainably."

Greenpalm's market data shows that palm oil certificates last traded at 30 cents and PKO certificates trade at $3.90.

Source: http://www.greenpalm.org/en/home, accessed 6 September 2011.

Khor Reports comment: The 30 cents premium is a big come down from the near USD40 price premium that certified sustainable palm oil (CSPO) first traded at. Arguably, Greenpalm's price is the most important single market indicator for the demand for sustainable palm oil, which is so far only available under the Roundtable for Sustainable Palm Oil (RSPO) initiative. The price collapse, of about 99%, indicates an excess of supply over demand for the RSPO's CSPO. At 30 cents per metric tonne of CSPO, there is scant hope for additional income for those operating sustainably. Most of the largest palm oil growers are heavily committed to RSPO certification and they will be hoping that this lead price indicator picks up. Palm oil sustainability experts often estimate the cost of RSPO certification at USD6-12 per metric tonne for corporate growers. Smallholders have been slower to get onto the programme; growers often say that a fair premium is needed to help this group. Sustainability practitioners point out that it may not be so difficult for this group to participate; but they need a change of mind-set and a dash of pride and hope. Although the market for sustainability seems to deliver a "no" - let's hope that is a temporary message.

Greenpalm's market data shows that palm oil certificates last traded at 30 cents and PKO certificates trade at $3.90.

Source: http://www.greenpalm.org/en/home, accessed 6 September 2011.

Khor Reports comment: The 30 cents premium is a big come down from the near USD40 price premium that certified sustainable palm oil (CSPO) first traded at. Arguably, Greenpalm's price is the most important single market indicator for the demand for sustainable palm oil, which is so far only available under the Roundtable for Sustainable Palm Oil (RSPO) initiative. The price collapse, of about 99%, indicates an excess of supply over demand for the RSPO's CSPO. At 30 cents per metric tonne of CSPO, there is scant hope for additional income for those operating sustainably. Most of the largest palm oil growers are heavily committed to RSPO certification and they will be hoping that this lead price indicator picks up. Palm oil sustainability experts often estimate the cost of RSPO certification at USD6-12 per metric tonne for corporate growers. Smallholders have been slower to get onto the programme; growers often say that a fair premium is needed to help this group. Sustainability practitioners point out that it may not be so difficult for this group to participate; but they need a change of mind-set and a dash of pride and hope. Although the market for sustainability seems to deliver a "no" - let's hope that is a temporary message.

Tuesday, August 30, 2011

Sarawak NCR land - a new development model

News article, 29 Aug 2011: "Felcra-like model to develop native land in S'wak"

Sarawak has introduced a new land management system modelled after Federal Land Consolidation and Rehabilitation Authority (Felcra) Bhd to develop Native Customary Rights (NCR) land in the state..... According to state land development minister Tan Sri Dr James Masing, the pilot project involving the new land management model was carried out in Pasai Siong, near Sibu......"The agreement with Felcra was reached in June this year. This is the first time we used this model on the NCR land management. This model has been used by Felcra in other land areas under the Ladang Rakyat scheme, but this is the first time it was applied to NCR land.... "This is because, to develop NCR land, you need the consent of landowners. Felcra will manage this pilot project with a fee for 15 years," he said.... under the new land management model, NCR landowners would hold 90% shares, with the remainder to be held by Sarawak Land Custody Development Authority (LCDA). Felcra will source all the funding required and will only charge management and marketing fees.... (source: http://thestar.com.my/news/story.asp?file=/2011/8/29/nation/20110829111929&s)

Khor Reports comments:

a) This is a promising new proposal for NCR land development in Sarawak. This is an advancement from the Sime Darby land deal proposals in FY2009, where the plantation sought a 60% stake, while offering the native landowners 30% and LCDA/Pelita 10%.

b) Previously, oil palm land deals have been in the eastern state of Malaysia have been problematic in their general poor inclusion of native landowners. Such issues are exemplified in the IOI Pelita case where a secondary land purchase has been bogged down by controversy from the initial land deal.

c) This suggests that any plantation should be concerned about the level of inclusion of local and native peoples in their current and existing projects. This "social agenda" is likely to become a significant issue for plantations.

d) Investors in plantations might become more keen to ask plantation companies to better disclose such risks, as well as the conservation / environmental usability and risks of their land banks.

Also view: http://khorreports-palmoil.blogspot.com/2011/04/native-customary-rights-ncr-issues-at.html

Sarawak has introduced a new land management system modelled after Federal Land Consolidation and Rehabilitation Authority (Felcra) Bhd to develop Native Customary Rights (NCR) land in the state..... According to state land development minister Tan Sri Dr James Masing, the pilot project involving the new land management model was carried out in Pasai Siong, near Sibu......"The agreement with Felcra was reached in June this year. This is the first time we used this model on the NCR land management. This model has been used by Felcra in other land areas under the Ladang Rakyat scheme, but this is the first time it was applied to NCR land.... "This is because, to develop NCR land, you need the consent of landowners. Felcra will manage this pilot project with a fee for 15 years," he said.... under the new land management model, NCR landowners would hold 90% shares, with the remainder to be held by Sarawak Land Custody Development Authority (LCDA). Felcra will source all the funding required and will only charge management and marketing fees.... (source: http://thestar.com.my/news/story.asp?file=/2011/8/29/nation/20110829111929&s)

Khor Reports comments:

a) This is a promising new proposal for NCR land development in Sarawak. This is an advancement from the Sime Darby land deal proposals in FY2009, where the plantation sought a 60% stake, while offering the native landowners 30% and LCDA/Pelita 10%.

b) Previously, oil palm land deals have been in the eastern state of Malaysia have been problematic in their general poor inclusion of native landowners. Such issues are exemplified in the IOI Pelita case where a secondary land purchase has been bogged down by controversy from the initial land deal.

c) This suggests that any plantation should be concerned about the level of inclusion of local and native peoples in their current and existing projects. This "social agenda" is likely to become a significant issue for plantations.

d) Investors in plantations might become more keen to ask plantation companies to better disclose such risks, as well as the conservation / environmental usability and risks of their land banks.

Also view: http://khorreports-palmoil.blogspot.com/2011/04/native-customary-rights-ncr-issues-at.html

Monday, August 1, 2011

Behemoths' land banking efforts stutter?

"Sime Darby’s expansion into Liberia may have hit some road blocks. It was reported that citizens from more than 15 towns and villages near Sime Darby Plantation in Grand Cape Mount County have threatened that the company would face stiff resistance if it intends any further extension of its concession. Not yet known at this point is the size of the area affected as portion to Sime’s 200,000ha concession land." (ECMLibra research report, 18 July 2011)

Khor Reports comments:

a) SE Asian plantations have taken a great interest in West Africa, Papua and other 'tougher' regions, to extend their land banks. Various problems have been reported with these major expansion efforts.

b) Sime Darby is reported facing some resistance from locals in Liberia (article above). The plantation behemoth had also sought to extend its interests in Sarawak, Malaysia, by offering larger stakes to local landholders - but we hear that some of these efforts may have gone 'on hold' for various reasons.

c) Golden Agri is also looking to develop 220,000 ha in Liberia via the USD1.6 billion deal with Golden Veroleum (the land area was initially reported as a 500,000‐acre palm oil plantation in the southeast of the country).3 September 2010: Golden Agri said its “subsidiary Golden VerOleum would form a partnership with the Government of Liberia in a palm oil project… for the cultivation of sustainable palm oil by the company and by Liberian smallholders and farmers, mill processing and value‐added manufacturing…The investment is expected to total USD1.6 billion” (source: http://www.reuters.com/article/2010/09/03/goldenagri‐liberia‐idUSSGC00373720100903). In October 2010. Golden Agri reported it disposed of its entire shareholding comprising one share of HK$1 in Golden Veroleum Limited. A clear status update is needed.

d) Sometime in 2009‐2010, Golden Agri’s “in progress” acquisition of 1 million ha in Papua falls through. Now, players like Wilmar are looking to Papua for major cane sugar projects. Will they have a happier outcome in the low-lying and seawater-flood prone region?

Khor Reports comments:

a) SE Asian plantations have taken a great interest in West Africa, Papua and other 'tougher' regions, to extend their land banks. Various problems have been reported with these major expansion efforts.

b) Sime Darby is reported facing some resistance from locals in Liberia (article above). The plantation behemoth had also sought to extend its interests in Sarawak, Malaysia, by offering larger stakes to local landholders - but we hear that some of these efforts may have gone 'on hold' for various reasons.

c) Golden Agri is also looking to develop 220,000 ha in Liberia via the USD1.6 billion deal with Golden Veroleum (the land area was initially reported as a 500,000‐acre palm oil plantation in the southeast of the country).3 September 2010: Golden Agri said its “subsidiary Golden VerOleum would form a partnership with the Government of Liberia in a palm oil project… for the cultivation of sustainable palm oil by the company and by Liberian smallholders and farmers, mill processing and value‐added manufacturing…The investment is expected to total USD1.6 billion” (source: http://www.reuters.com/article/2010/09/03/goldenagri‐liberia‐idUSSGC00373720100903). In October 2010. Golden Agri reported it disposed of its entire shareholding comprising one share of HK$1 in Golden Veroleum Limited. A clear status update is needed.

d) Sometime in 2009‐2010, Golden Agri’s “in progress” acquisition of 1 million ha in Papua falls through. Now, players like Wilmar are looking to Papua for major cane sugar projects. Will they have a happier outcome in the low-lying and seawater-flood prone region?

Cargill goes RSPO but keeps smallholders in

Cargill has announced that the palm oil products it supplies to its customers in

Europe, United States, Canada, Australia and New Zealand will be certified by the

RSPO and/or originated from smallholder growers by 2015. This commitment will

be extended across all Cargill's oil and trading businesses to cover 100% of its palm

oil products and all customers worldwide – including China and India – by 2020.

Khor Reports comment:

Cargill includes the smallholder element with the “and/or” flexibility for its sourcing. This seems a tacit acknowledgment that RSPO may have problems including smallholders in its efforts to a significant degree. With Greenpalm certs just bouncing off a meager $1 per unit, it seems hard for smallholders to see monetary compensation for their RSPO certification efforts, unless an attractive program for them is launched soon. The biggest concern we have had with regard to RSPO is its de facto limited inclusion of independent smallholders thus far. We think Cargill’s move is pragmatic and heartening in terms of keeping market access open for these smallholders.

Europe, United States, Canada, Australia and New Zealand will be certified by the

RSPO and/or originated from smallholder growers by 2015. This commitment will

be extended across all Cargill's oil and trading businesses to cover 100% of its palm

oil products and all customers worldwide – including China and India – by 2020.

Khor Reports comment:

Cargill includes the smallholder element with the “and/or” flexibility for its sourcing. This seems a tacit acknowledgment that RSPO may have problems including smallholders in its efforts to a significant degree. With Greenpalm certs just bouncing off a meager $1 per unit, it seems hard for smallholders to see monetary compensation for their RSPO certification efforts, unless an attractive program for them is launched soon. The biggest concern we have had with regard to RSPO is its de facto limited inclusion of independent smallholders thus far. We think Cargill’s move is pragmatic and heartening in terms of keeping market access open for these smallholders.

Malaysia criticizes "sinister" campaign against palm oil

The Malaysian Insider reports: “It is utter cruelty to the orang utans. The zoo must understand these are animals from the tropics and adequate protection should be given to them during winter. Their enclosures must be warm and made comfortable,” (Tan Sri Yusof Barison, head of the Malaysia Palm Oil Council) was quoted as saying..... Yusof was reported as saying that he suspects having the orang utans in such degrading captivity was to win public support in Australia in the campaign against the use of palm oil products.... He said having anti-palm oil signs at the zoo was to win public sympathy and to misrepresent the orang utan issue.... “Australians must visit our orang utan sanctuaries in Malaysia and see how well the animals are taken care of. There is something sinister behind the campaign by western NGOs to ruin the palm oil industry,” he said. (Source: http://www.themalaysianinsider.com/malaysia/article/palm-oil-council-chief-upset-over-orang-utan-treatment-in-aussie-zoo/)

Khor Reports comment: The orang utan is a key symbol of the campaigns by NGOs for the sustainable growing of palm oil i.e. without deforestation, peat land development and loss of biodiversity.

Khor Reports comment: The orang utan is a key symbol of the campaigns by NGOs for the sustainable growing of palm oil i.e. without deforestation, peat land development and loss of biodiversity.

Tuesday, July 5, 2011

Trends in planted area for the Top 10

Khor Reports comment: The recent 3-year expansion by the ten largest plantations has averaged some 18,000 ha each year. The annual net increase in their planted area has decelerated from an average of 33,000 to11,300 and 9,300 ha per year. The recent Indonesian moratorium on deforestation has been successfully diluted by corporate and development lobbies. Indonesian planters note that uncertainty surrounding the moratorium had the impact of tamping back their country's 2010 expansion to some 300,000 ha instead of a minimum 500,000 ha per year in prior years (refer to http://khorreports-palmoil.blogspot.com/2011/05/indonesia-moratorium-eases-business-and.html ). Indonesia is widely reported as deforesting at the rate of 1 million ha per year. This implies that oil palm new plantings accounts for half of Indonesia's recent annual deforestation.

Sunday, May 22, 2011

The Top 30

The Top 30 public-listed SE Asian plantation groups, listed by market capitalization:

Source: Khor Reports

Data: Bloomberg, 27 Jan 2011

The aggregate landbank (hectares) for selected top plantation groups (inclusive own estates, smallholder / plasma, interest in joint ventures, and unplanted areas):

Source: Khor Reports

Data: Recent company annual reports

Source: Khor Reports

Data: Bloomberg, 27 Jan 2011

The aggregate landbank (hectares) for selected top plantation groups (inclusive own estates, smallholder / plasma, interest in joint ventures, and unplanted areas):

Source: Khor Reports

Data: Recent company annual reports

Indonesia moratorium eases business and growth concerns

"Moratorium issued to protect primary forests, peatland" May 20, 2011 14:01 PM, The Jakarta Post, http://www.thejakartapost.com/news/2011/05/20/moratorium-issued-protect-primary-forests-peatland.html

Excerpts:

President Susilo Bambang Yudhoyono on Thursday finally signed a policy banning the conversion of primary forest and peatland for two years as part of a government pledge to combat climate change through reducing deforestation..... With the presidential instruction, all local authorities should stop issuing forestry permits, including for plantation and mining companies eyeing businesses in primary forest and peatland areas.

“The moratorium will apply to 64 million hectares of forests across the country,” Agus Purnomo, the President’s aide on climate change issues, said.... However, most of the 64 million hectares .... is located in areas already protected by the 1999 Forestry Law.... “We are double protecting these protected areas since in fact many of these areas are still prone to deforestation. We hope the moratorium will help better protect the forests,” Agus said.

He said businesspeople could still expand into the 34 million hectares categorized as degraded forest areas.... The presidential decree still allows the exploitation of peatland with a depth of less than three meters.

Indonesia has the world’s third-largest expanse of forest with 120 million hectares of rainforest, 40 million of which are protected forest and conservation areas that cannot be exploited for commercial purposes.

According to a letter of intent with Norway, Indonesia is required to stop issuing new permits for exploiting natural forests and peatland within two years.... In return, Indonesia would receive money based on the total amount of carbon emissions reduced within the two years.

Indonesian Environmental Forum (Walhi) senior campaigner Teguh Surya said the government had betrayed its promise to protect forests by only banning the conversion of primary forests and peatland rather than all naturals forests.... “The President ignored input from civil society who care about conserving forests and threw its support to big businesses, such as palm oil plantations,” he told the Post.

.....................................

The business reaction:

"I appealed to the government that non-forest areas should not be included in the moratorium," said Joko Supriyono, secretary general at the Indonesian Palm Oil Association (Gapki). "The impact of the moratorium, even though they postponed the signing, was uncertainty," he told Reuters. He said this uncertainty had led to expansion in 2010 of 300,000 hectares of palm oil plantations in the world's top palm oil producing nation, reduced from a minimum 500,000 hectares in recent years...." Source: Reuters news article.

"Presidential Adviser on climate change, Agus Purnomo said that there would be no new permits on 64 million ha of land in Indonesia. The silver lining is that the moratorium will exempt the extension of old permits, projects given permits in principle by the forestry ministry and issuance of permits to log onsecondary non-peatland forests or convert degraded land. The moratorium will also exempt projects for the development of energy supplies as well as a huge food plantation project in Papua province. We view this development positively as previously, there were worries that the new version of the moratorium may affect plantation companies with “Hak Izin Lokasi” land permits... which is obtained before the “Hak Guna Usaha” (HGU) permit is granted. HGU is land rights granted for 35 years and can be extended for another 25 years. Clearance of land is permitted with “Hak Izin Lokasi”...." Source: "Plantation Sector (Overweight): Indonesia signs moratorium on forest clearing finally," AmResearch, 20 May 2011.

Khor Reports comment:

a) The moratorium was due to start January 2011, but was delayed five months. It is a REDD+ effort to reduce greenhouse gas emissions from deforestation under a USD1 billion deal with Norway. There was widely reported disagreement between the ministries in Indonesia on how extensive the ban on forest clearing should be. The indicators were clear in recent months that a more pro-business stance would likely be adopted.

Businesses will be looking out for land bank:

i) Secondary forest lands for development, including:

34 million hectares categorized as degraded forest areas; and

Peatland with a depth of less than three meters.

ii) Land for development in Papua

b) In 2003, the Indonesian authorities estimated that the potential area for oil palm is 24.5 million hectares. By region, the recent planted (2009) and potential areas are: Sumatra 5.2 and 7.2 million ha (+2); Java 0.02 and 0.3 million ha (+ 0.28), Kalimantan 1.9 and 10.3 million ha (+8.4), Sulawesi 0.2 and 0.4 million ha (+0.2) and Papua 0.06 and 6.3 million ha (+6.24).

c) However, NGO pressures to reduce the rapid expansion of oil palm development in Indonesia have taken their toll. Indonesia's 2-year moratorium on deforestation starts May 2011. It prohibits development on primary forest and deep peat lands (but secondary forest and Papua is exempt from the restriction). The 2003 study likely included areas, which are now considered unsuitable for development for environmental reasons. The potential areas for Kalimantan and Sumatra could be revised down, but those for Papua remain intact.

d) Rapid oil palm development has raised the concern of deforestation in Indonesia. NGOs have been campaigning against new plantings in all types of forested areas and peat lands. While the pro-business outcome of the environment vs. development tussle (over the details of Indonesia's 2-year moratorium on deforestation) may not slow the pace of development by commercial estate owners, successful NGO campaigning with global palm oil buyers such as Nestle and Unilever may have an impact on the largest integrated plantation groups. So far NGO campaigning has been targeted at the top few.

The recent Golden Agri (Sinar Mas) - The Forest Trust deal is noteworthy. The oil palm giant promises not to develop lands with more than 35 tonnes carbon per hectare. Will such voluntary bilateral deals and the efforts of the RSPO hamper expansion efforts of only the largest public-listed groups, or will they extend their reach beyond these to have some real impact on the continued go-go expansion of oil palm hectarage?

Excerpts:

President Susilo Bambang Yudhoyono on Thursday finally signed a policy banning the conversion of primary forest and peatland for two years as part of a government pledge to combat climate change through reducing deforestation..... With the presidential instruction, all local authorities should stop issuing forestry permits, including for plantation and mining companies eyeing businesses in primary forest and peatland areas.

“The moratorium will apply to 64 million hectares of forests across the country,” Agus Purnomo, the President’s aide on climate change issues, said.... However, most of the 64 million hectares .... is located in areas already protected by the 1999 Forestry Law.... “We are double protecting these protected areas since in fact many of these areas are still prone to deforestation. We hope the moratorium will help better protect the forests,” Agus said.

He said businesspeople could still expand into the 34 million hectares categorized as degraded forest areas.... The presidential decree still allows the exploitation of peatland with a depth of less than three meters.

Indonesia has the world’s third-largest expanse of forest with 120 million hectares of rainforest, 40 million of which are protected forest and conservation areas that cannot be exploited for commercial purposes.

According to a letter of intent with Norway, Indonesia is required to stop issuing new permits for exploiting natural forests and peatland within two years.... In return, Indonesia would receive money based on the total amount of carbon emissions reduced within the two years.

Indonesian Environmental Forum (Walhi) senior campaigner Teguh Surya said the government had betrayed its promise to protect forests by only banning the conversion of primary forests and peatland rather than all naturals forests.... “The President ignored input from civil society who care about conserving forests and threw its support to big businesses, such as palm oil plantations,” he told the Post.

.....................................

The business reaction:

"I appealed to the government that non-forest areas should not be included in the moratorium," said Joko Supriyono, secretary general at the Indonesian Palm Oil Association (Gapki). "The impact of the moratorium, even though they postponed the signing, was uncertainty," he told Reuters. He said this uncertainty had led to expansion in 2010 of 300,000 hectares of palm oil plantations in the world's top palm oil producing nation, reduced from a minimum 500,000 hectares in recent years...." Source: Reuters news article.